Yes, we’ve still got an issue with slow growth around the world, finds NAB’s Alan Oster. And we can expect more of the same for a while still. But there are brighter spots for the Australian economy, and with that, emerging opportunities for businesses.

Here’s what we heard when Alan took us through the bank’s data and modelling on the global and local economy.

Here’s what we heard when Alan took us through the bank’s data and modelling on the global and local economy.

Watch the webinar

Growing pains for the global economy

It’s a complex and concerning time in international affairs, and in turn, the global economy.

Conflicts in Ukraine and the Middle East are buffeting commodity and trade markets, while potential fallout from regional tensions around China remains difficult to predict.

Beyond geo-political matters, Alan shared a series of economic data showing that “the world is not your friend”. There’s been a broad economic slowdown in major economies on the back of central bank efforts to tame inflation. The effect of increased rates is taking its desired effect – and hurting growth. Major manufacturing economies, like Germany and China, have taken a hit and consumers aren’t spending. America has been an exception – though it won’t be immune, with Alan anticipating the US will have its turn later this year.

While interest rate cuts are expected to begin trickling through international markets over the coming 12 months, the global growth forecast for 2024 is just 2.9%. Then, just marginal increases in 2025 and 2026.

Conflicts in Ukraine and the Middle East are buffeting commodity and trade markets, while potential fallout from regional tensions around China remains difficult to predict.

Beyond geo-political matters, Alan shared a series of economic data showing that “the world is not your friend”. There’s been a broad economic slowdown in major economies on the back of central bank efforts to tame inflation. The effect of increased rates is taking its desired effect – and hurting growth. Major manufacturing economies, like Germany and China, have taken a hit and consumers aren’t spending. America has been an exception – though it won’t be immune, with Alan anticipating the US will have its turn later this year.

While interest rate cuts are expected to begin trickling through international markets over the coming 12 months, the global growth forecast for 2024 is just 2.9%. Then, just marginal increases in 2025 and 2026.

But, in Australia

Things are looking a bit better.

While we haven’t avoided the impacts of higher interest rates and a slowing global economy, the general outlook over the coming period holds reason for optimism.

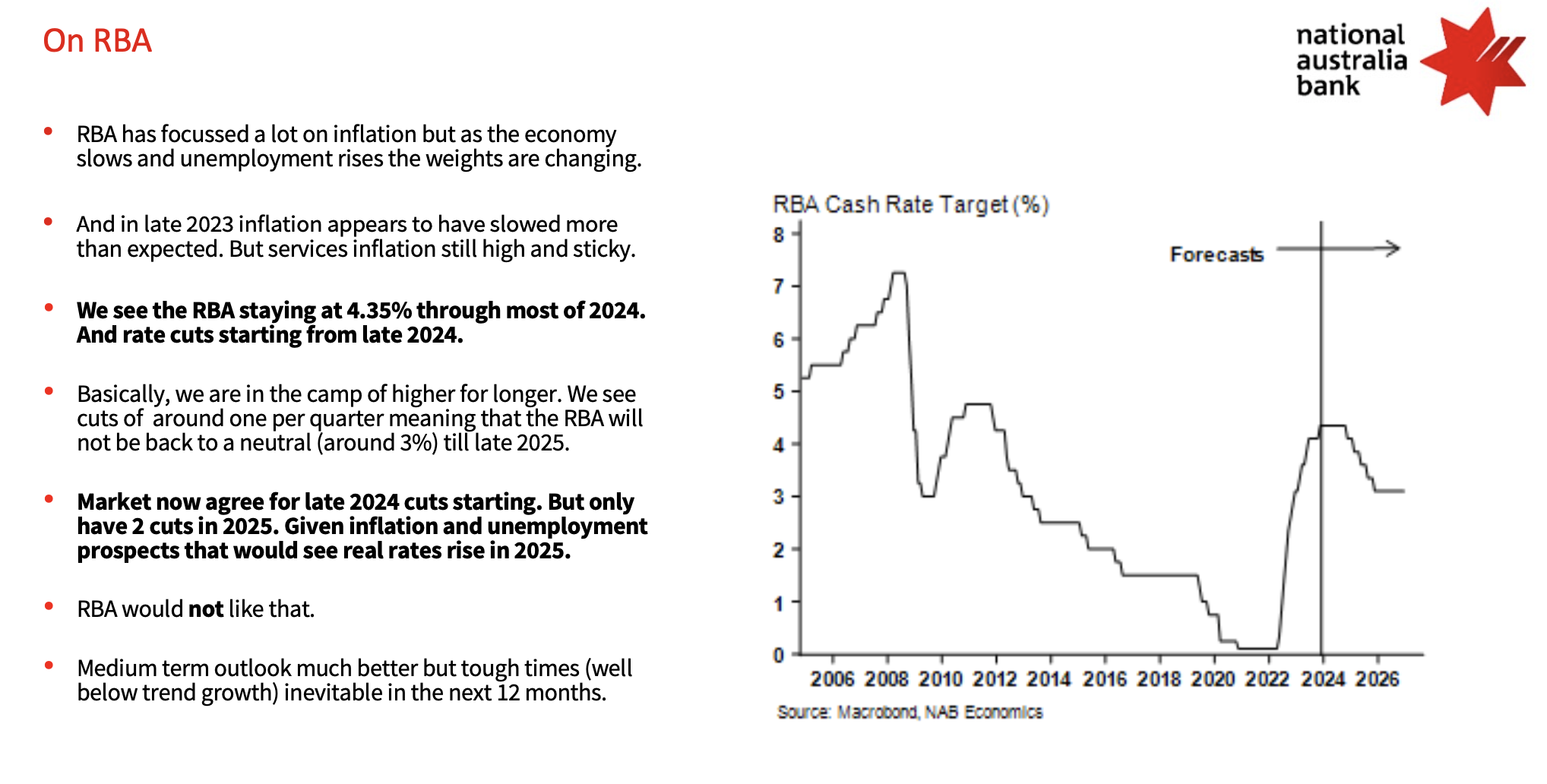

At the time of this webinar, 23 April, the NAB was anticipating inflation to fall to 3% by the end of the year, and 2.5% in 2025. With this, a long-awaited rate cut by the RBA could greet punters on Melbourne Cup Day. This will be heartening for many SMEs. Things may alter slightly with the recent inflation figures announced on 24 April being higher than market analysts predicted. Although many businesses have adapted to this ‘new normal’ of high costs, inflation is still hurting businesses. As well as being a prominent response in NAB’s surveys, Banjo’s latest SME Compass report found that inflation is a pain-point for about 40% of operators – and something that’s impacting their growth.

After crawling through this year, NAB also sees economic growth returning to trend by late 2025, and jobs growth remaining robust, albeit not at a rate to stop unemployment drifting towards 4.5%.

Collectively, it’s a medium-term picture that Alan thinks would be the envy of many countries in the world.

While we haven’t avoided the impacts of higher interest rates and a slowing global economy, the general outlook over the coming period holds reason for optimism.

At the time of this webinar, 23 April, the NAB was anticipating inflation to fall to 3% by the end of the year, and 2.5% in 2025. With this, a long-awaited rate cut by the RBA could greet punters on Melbourne Cup Day. This will be heartening for many SMEs. Things may alter slightly with the recent inflation figures announced on 24 April being higher than market analysts predicted. Although many businesses have adapted to this ‘new normal’ of high costs, inflation is still hurting businesses. As well as being a prominent response in NAB’s surveys, Banjo’s latest SME Compass report found that inflation is a pain-point for about 40% of operators – and something that’s impacting their growth.

After crawling through this year, NAB also sees economic growth returning to trend by late 2025, and jobs growth remaining robust, albeit not at a rate to stop unemployment drifting towards 4.5%.

Collectively, it’s a medium-term picture that Alan thinks would be the envy of many countries in the world.

What about SMEs?

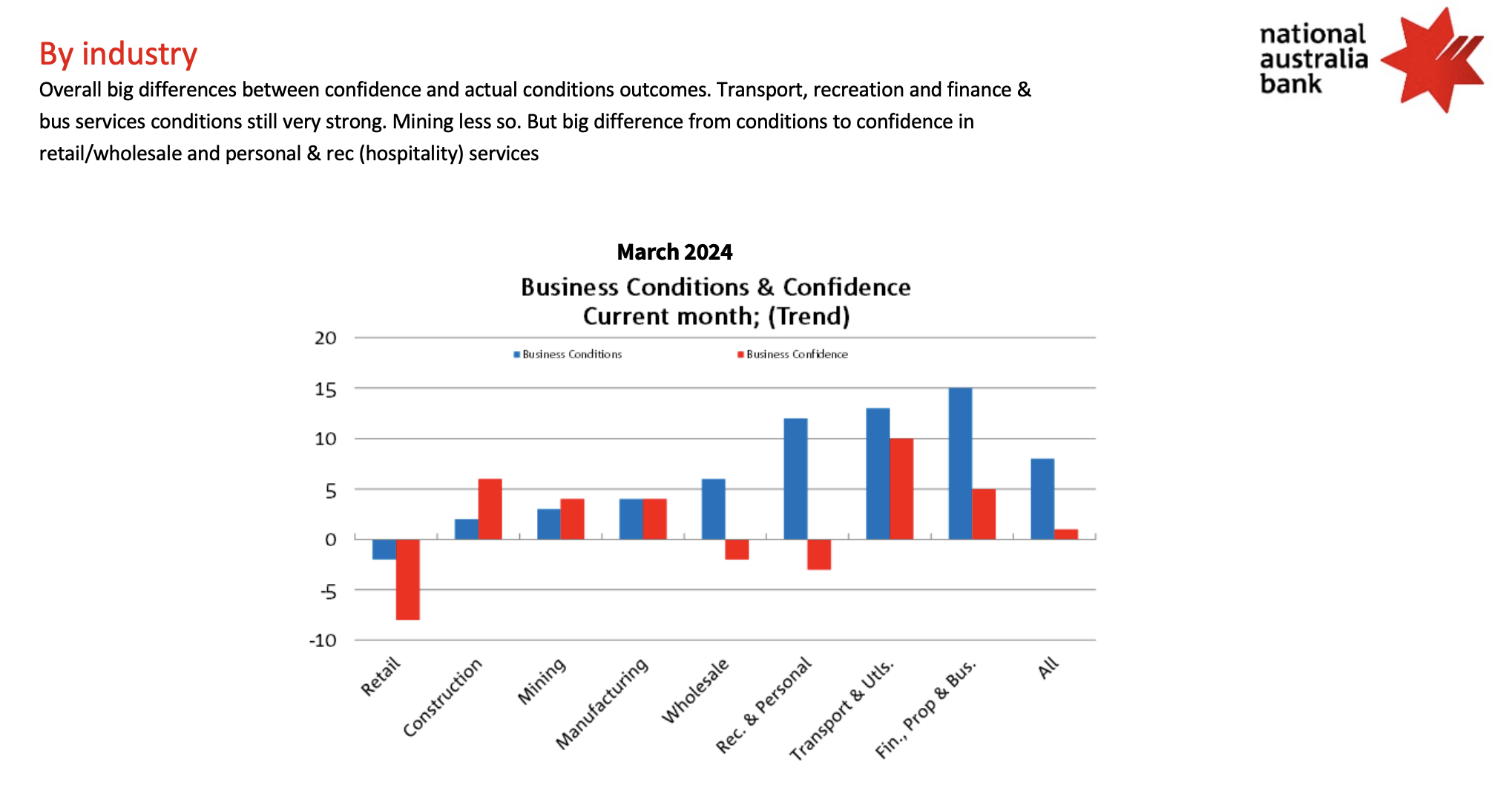

And with these bright spots for the economy, there are also signs that businesses are gaining confidence – but not all, and not consistently. Indeed, there’s a real split in how different sectors, and states, are going.

NAB’s latest business survey shows healthy confidence levels among transport, finance and business services, and improved outlooks within mining and manufacturing industries. At the same time, optimism has vanished from retailers, and confidence is lower among wholesale and hospitality sectors.

Similarly, there’s great variation in forward orders and business conditions.

It’s something reflected in our March quarter Banjo Barometer, where loan applications were down for retailers and wholesalers, but on the up for transport and manufacturing sectors.

NAB’s latest business survey shows healthy confidence levels among transport, finance and business services, and improved outlooks within mining and manufacturing industries. At the same time, optimism has vanished from retailers, and confidence is lower among wholesale and hospitality sectors.

Similarly, there’s great variation in forward orders and business conditions.

It’s something reflected in our March quarter Banjo Barometer, where loan applications were down for retailers and wholesalers, but on the up for transport and manufacturing sectors.

And it’s something that Alan notes in plans for how SMEs will price their product. Where 2023 saw businesses aiming to keep their profit margins, this year it's about maintaining market share.

In fact, ‘keeping the lights on’ is a real focus, with NAB finding that 35% of SMEs are most worried about staff turnover and labour and 34% concerned about cashflow.

In fact, ‘keeping the lights on’ is a real focus, with NAB finding that 35% of SMEs are most worried about staff turnover and labour and 34% concerned about cashflow.

A 'Tay Tay' spending model

The flow of cash from consumers is also confounding.

While experiences of financial hardship have been rising, and cost of living remains their key concern, Alan notes that consumers will still “spend when they want to”, with a case-in-point being people buying expensive tickets to see a Taylor Swift concert. (Alan noted that of the 0.3% retail sales in February, 0.2% was associated with the Taylor Swift tour!).

On other fronts, there’s been a quarterly bounce in expectations for making major purchases in the coming year. However, this doesn’t appear likely to come via the Stage 3 tax cuts, with NAB finding more than 50% of taxpayers will save the extra money and pay down debt.

Supporting consumers to shake off this defensive position will be on the minds of the RBA as the focus shifts from fighting inflation to stimulating the economy.

And with that, Alan sees a run of rate cuts through 2025, along with a return to target ranges for Australia’s major economic indicators.

While experiences of financial hardship have been rising, and cost of living remains their key concern, Alan notes that consumers will still “spend when they want to”, with a case-in-point being people buying expensive tickets to see a Taylor Swift concert. (Alan noted that of the 0.3% retail sales in February, 0.2% was associated with the Taylor Swift tour!).

On other fronts, there’s been a quarterly bounce in expectations for making major purchases in the coming year. However, this doesn’t appear likely to come via the Stage 3 tax cuts, with NAB finding more than 50% of taxpayers will save the extra money and pay down debt.

Supporting consumers to shake off this defensive position will be on the minds of the RBA as the focus shifts from fighting inflation to stimulating the economy.

And with that, Alan sees a run of rate cuts through 2025, along with a return to target ranges for Australia’s major economic indicators.