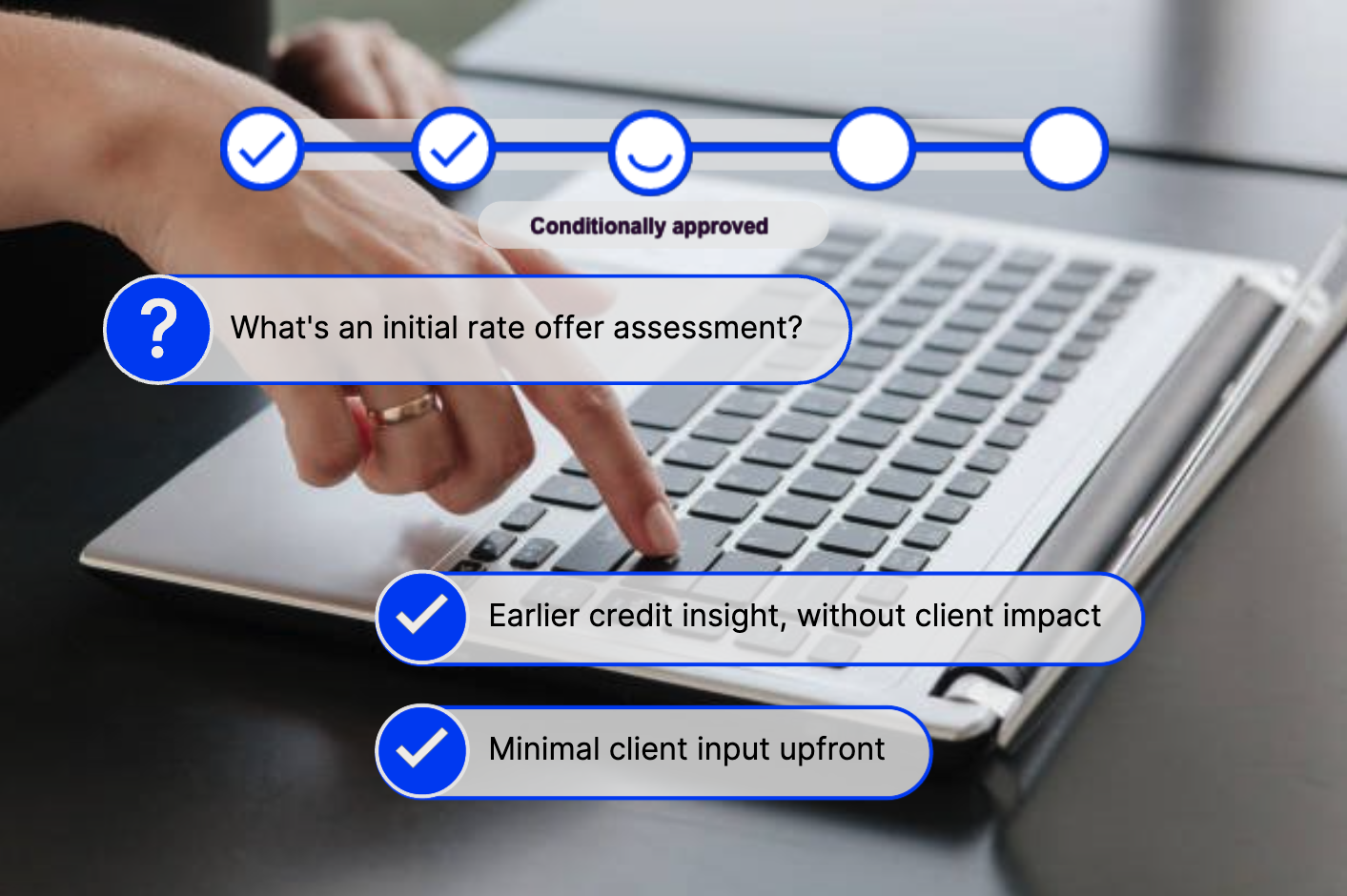

Earlier credit insight, without client impact.

When you’re assessing a deal, speed and certainty matter, but so does protecting your client’s credit profile. Banjo’s partner application process is designed to help you quickly check eligibility and pricing early, so you can strengthen client rapport and move forward with confidence.

Below is a clear overview of how Banjo’s Partner application process works, what it includes, and answers to common questions brokers ask.

Frequently asked questions about our assessment process

What is an initial rate offer assessment?

An initial rate offer assessment within Banjo’s application process enables brokers to enquire to check their clients’ suitability, assess potential deals, and reach a conditional approval with indicative terms. All without requiring deep client involvement or impacting their credit score.

Does the initial rate offer assessment affect my client’s credit score?

No. The initial credit check for rate offer purposes leaves no footprint and has no impact on your client’s credit score. It’s designed to help you assess a potential deal with confidence, without creating any adverse credit activity for the client.

Do I need my client involved to run the initial rate offer assessment?

No. If your client has given you the ok in writing, you can complete the assessment independently. We’ll simply send them a notification email letting them know their broker has requested an initial rate offer assessment. The email clearly states that this assessment has no impact on their credit score and is purely to help progress their funding scenario.

What does the conditional approval include?

The conditional approval includes accurate, indicative terms based on the client’s eligibility and pricing profile. While not a final approval, it enables you to present a clear, informed potential funding path before proceeding to a full application.

What if my client chooses not to proceed?

Not a problem, the application can be withdrawn at any time.

When does a full credit check occur?

When an application is ready for formal loan assessment, a full credit check is undertaken with the borrower’s consent. This involves a detailed review of credit bureau information and financial details to validate disclosed liabilities, assess serviceability and confirm lending terms. The full credit check is required for approval and is recorded as an enquiry on the borrower’s credit file.

Banjo’s initial rate offer assessment is designed to support better broker conversations, earlier. It helps you test deal fit, set expectations with confidence, and progress the right opportunities without unnecessary friction. When you’re ready to move forward, the formal loan assessment is there to support the next step.

Get clarity before you proceed.

It doesn't take long and won't affect your clients credit score.